Is lifting the tax on individual income realistic or utopian? – a review of the Union Budget 2026

By Dr. A.Lakshmana Rao

Associate Professor &HoD

Dept. of Commerce – Paari School of Business,

SRM University – AP, Amaravati.

The system of imposing tax on subjects is a known phenomenon since ancient times, there were various forms of taxes that were imposed on people, property, goods and trade activities, there were evidences in Kautilya’s “Arthashastra” like taxes on land revenue and trade duties as early as in 300 BC itself, the form of tax is undergoing drastic form of reforms since then to today’s various forms of tax in the name of Direct Taxes and Indirect Taxes.

The structured form of imposing tax on individual income started in British regime during 1860 by passing the first Income Tax Act, 1860, there were later followed with 1866, 1922 and the current Indian Income Tax Act, 1961, which is going to be replaced with another new Income Tax Act, 2025, which will come into effect from 1st of April, 2026 as per the announcement made by the Finance Minister Ms. Nirmala Seetharaman, during her budget presentation on 1st February 2026. It needs a good applause, as it is always replacing old law a mammoth exercise.

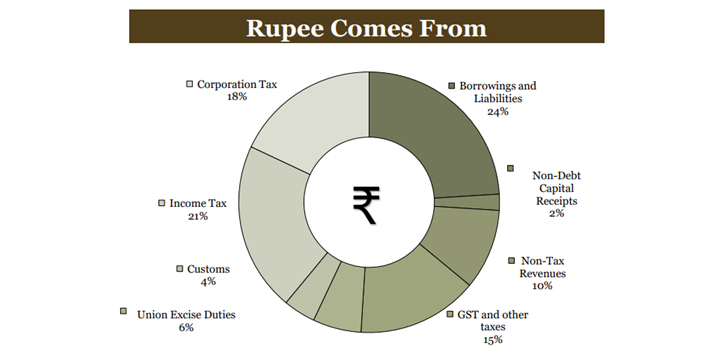

Therefore, it is noteworthy that starting from 1860 to till today individuals are subject to structured individual income tax. The Government’s major dependence on income tax as one of the sources of revenue is evidentiary. To understand it’s significance, we can have a look on Union Budget 2026 on, how rupee comes from

Source: Union Budget 2026-27

Out of the 100% sources from where rupees come, the major source of revenue is Income Tax with 21% (excluding 24% on borrowing and liabilities) later with 18% Corporate Tax, 15% GST and the others with the remaining. It shows the high reliance of Government on Income Tax. Individual income taxpayers, always expect tax incentives, however the Government has lot many considerations to its account in determining these incentives. The 2026 budget has benefited this group in a different way by extending the tax filing dates in the form of ITR-1 and ITR-2 till 31st July and for non-audit businesses, trusts the due date of filing extended till 31st August, for the revised tax returns the due date is extended from 31st December to 31st March. These will not have much impact on their tax payment. Therefore, we can say it is in one wayupset the individual taxpayers.

Reducing individual income tax rates requires some review, if we review, we can see primarily two contradictory elements, though it may apply to all the tax subjects/payers, which is as follows:

- Individuals always expects in each and every budget tax relief, and feels the money earned is their hard earned one, on the other hand

- The Government’s thrust is, how to gain the major source of revenue through tax by fulfilling various subjects’ interests leading to the development of the nation?

Accordingly, it could lead to a situation that, no tax no Government, though virtually any welfare Government may not be interested to taxits individuals, but its very existence is dependent on its tax resources.

To fulfil these ends, the tax planners of the Government comes with various innovative and thought provoking ideas to instil economic stability on one hand the public welfare on the other hand, at this juncture the Union Budget 2026 has not changed the tax slabs and individual income tax rates during 2026-27, this may be upsetting to the tax payers, however, there is a notable tax reduction in the form GST from its earlier various slabs into 0%, 5%, and 18% tax rates in September, 2025. There is always a scope to play with these rates and slabs by the Government, keeping in mind various economic, global and national political factors. With respect to Individual Income Tax, the 1997-98 considered as lowest ever after Independence and later 2005-06 were considered as tax heavens for individual income taxpayers.

However, if we see some of the economies other than India, there are countries from zero to low-income tax rates, there existence depends on other sources of income. There are countries, which are steadily reducing theirindividual income tax rates and paving the roads to zero income tax, the logic behind this notion is that, if the Government encourages the spending pattern of the individual, automatically it will boost the economy, because of the more disposable income, the individual will try to spend and try to earn more in different forms of investment leading to the wealth creation of all, this will enhance the economic system in the long run, and the complications of taxing and the load of the Government on focussing on tax evasion, will be reduced, consequently, it may lead to abolition of Income Tax Acts, and all the provisions and sections corresponding to the individual income as per the evidences from some of the countries.There are considerable arguments both in favour and opposition to taxing individual income. From our Indian perspective also, therewere some evidences not directly with respect to abolition of Income Tax Act but from the angle of creation of economic wealth, the abolition of MRTP Act, 1969 and the formation of The Competition Act, 2002.There were 73 full budgets produced in India after Independence, none of these budgets have mentioned, their intention or plan with respect to lifting of tax on individual income progressively or at least with some focus on it.

Taking cues from these changes and the tax systems of many other countries in the world with respect to individual income tax, whether the proposed new Income Tax Act, 2025, effective from 1st April, 2026 will lead to lifting of tax on individual income or will it be a utopian to expect in the years to come, may be at least by year 2047?

(The views expressed in this article are of those of the Author and not of the institution and not necessarily reflects the views of others)